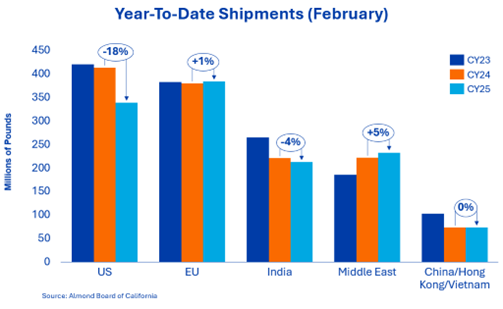

India shipped 41.3 million pounds in February, bringing year-to-date shipments to 213.1 million pounds, compared to 221.4 million pounds in the same period last year. This represents a year-on-year decline of around 4 %. Although the pace is slightly behind that of the previous year, demand factors in India remain favorable overall. Local inventory levels are considered relatively manageable and retail prices have remained stable in several key trading centers. However, buying activity has been somewhat mixed in recent weeks as importers monitor global price trends and general macroeconomic conditions. Market participants are also closely monitoring currency developments and potential political developments related to import tariffs, as both can influence buying behavior.

Shipments to China and Hong Kong totaled 3.3 million pounds in February, an increase of 144 % year-over-year. Shipments to Vietnam reached 6.0 million pounds, an increase of 155 % month-over-month and an impressive 72 % year-over-year. Combined shipments to these regions were up 151 % year-over-year in February, bringing the year-to-date total into positive territory for the first time this 2025 crop year at 0.34 %. This result is an encouraging sign of strengthening demand and continued momentum in these key markets.

Europe recorded another month of solid demand with shipments totaling 74.2 million pounds, continuing the trend for the year. Buyers continue to pursue a strategy of buying on demand, which should lead to continued demand for the remainder of the year. Spain and Italy continue to record strong growth of 16 % and 18 % respectively. Germany recorded a year-on-year decline of 2 %, but continues to provide a stable level of demand. While some markets on the continent remain cautious, overall demand from Europe continues to ensure stability on the export markets.

Shipments to the Middle East totaled 28.1 million pounds in February, bringing year-to-date shipments to 233.1 million pounds - an increase of approximately 5 % over last year. The region continues to be an important market for California almonds, supported by strong consumer demand and well-established trade channels. Turkey, Israel and Lebanon are performing better year-on-year, while Saudi Arabia, Jordan and Iraq are all experiencing double-digit year-on-year declines. Normally, the next week or two would be expected to see a restocking for Ramadan as buyers return to the market; however, with recent geopolitical developments in the region bringing additional uncertainties regarding logistics and trade flows, some of this demand may be lost. While the overall underlying demand across the Middle East remains stable, disruptions to shipping routes and schedules have caused short-term delays and required adjustments to freight planning and handling. Market participants are monitoring developments closely, while both sides of the trade are exploring alternative route options as required.

Shipments in February amounted to 45 million pounds, a decrease of 19.9 % compared to the same period last year. Demand in the domestic market continues to fall, with results down 18.1 % overall since the start of the year. New business performed well, with a year-on-year increase of 72 % resulting in forward contracts falling by only 1.1 %. This market continues to face multiple challenges, particularly reflected in categories such as snack almonds, which saw double-digit declines in the last quarter. Recent booking activity has allowed buyers to be patient when deciding when to cover the final stretch of this crop year.

Total commitments currently stand at £593 million, up £2.77 % on the previous year. New sales during the month totaled 246.3 million pounds, with the domestic market recording an additional 50.6 million pounds - an increase on last year's 29.4 million pounds.

Exports recorded an increase of 195.7 million pounds in new contracts, a slight increase on last year's 191.4 million pounds. Total commitments for the domestic market now stand at 220 million pounds, while exports have reached 374 million pounds to cover upcoming deliveries. Uncommitted stocks have increased by 3.5 % on the previous year and stand at 999 million pounds compared to 965 million pounds.

Crop receipts were surprisingly high in February and now stand at 2.68 billion pounds, indicating an updated final crop size of approximately 2.71 billion pounds. This puts the industry's final 2025 crop at a similar level to the 2024 crop. February's weather in California's growing regions brought a mix of varying temperatures and intermittent storms during the critical flowering period.

Flowering progressed rapidly from the beginning of February to the end of the month, with isolated rain and wind events restricting bee flight and pollination activity. However, the warmer and drier conditions towards the end of the month helped the orchards to pass through the flowering phase and move into the flower drop phase, encouraging early nut development. At this early stage, it is still too early to draw any definitive conclusions about crop size. Over the next two months, the trees will shed non-viable nuts, which will give an indication of the harvest potential. As the nuts begin to ripen, the weather will be a critical factor in crop development. Growers will be keeping an eye on water availability as we enter the warmer months of the year and adjusting their operations accordingly.

February's situation report provided an encouraging signal for the market: total shipments amounted to 241.1 million pounds, an increase of 12 % year-on-year, primarily due to strong export demand. The shipment figures show that global buyers continue to be responsive when prices are in line with market expectations, particularly in key export destinations. Export markets continue to be the primary driver of industry performance, offsetting weaker domestic demand and underscoring the importance of international trade channels for California almonds. The fundamentals of this latest report should ensure price stability.

With flowering now complete in California's growing regions, the industry's focus in the coming weeks will increasingly turn to early plant development and initial assessments of fruit set. Together with the shipping rhythm and the global demand situation, the course of the 2026 harvest will continue to shape market sentiment as the industry enters the second half of the marketing year.

Senior Sales Director Nut Ingredients