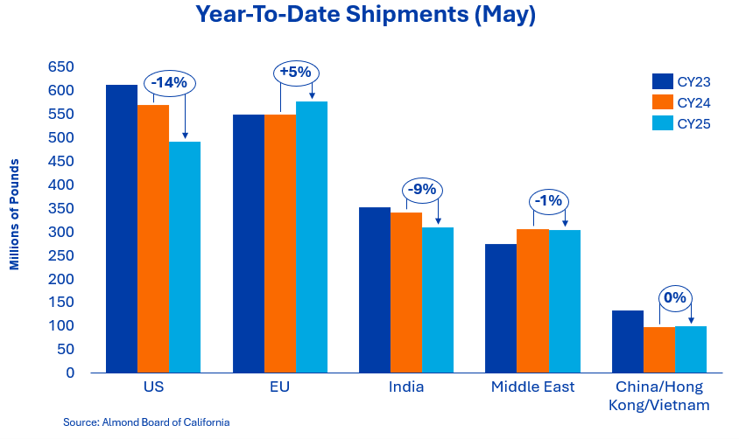

India remains a closely watched market. While shipments continue to trail last year’s pace by approximately 9%, buyers remain active and continue to extend coverage as needed. Currency pressures, elevated replacement costs, and a weaker Indian Rupee have shaped purchasing behavior throughout much of the season, resulting in a generally disciplined, hand-to-mouth buying approach. Despite these challenges, India continues to demonstrate its importance to California almonds, with market participants reporting generally balanced inventories and ongoing demand. Looking ahead, seasonal demand patterns and future coverage decisions will remain key factors influencing shipment activity during the last few months of the crop year.

China & Hong Kong shipments increased 5% compared to May of last year however, year-to-date shipments remain down 37%. In contrast, Vietnam continues to perform strongly, with shipments up 36% year to date. As a result, the combined performance of the two regions is slightly positive, up 0.5% overall.

The ongoing tariff situation in China continues to hinder sales growth in the region. While the May 14–15 summit between U.S. President Donald Trump and Chinese President Xi Jinping was initially viewed as a positive development, it ultimately did not result in the new tariff agreements that many had hoped would improve the trade conditions. China will continue to be a market of interest as buyers evaluate supply options for the upcoming season. Industry discussions suggest quality concerns within portions of the Australian crop may influence purchasing decisions and increase consideration of California origin almonds. While it remains early to quantify the full impact, market participants will continue monitoring trade flows into the region as new crop shipments begin.

Europe continues to provide a solid foundation for global demand, with shipments to the region running ahead of last year by 5%. Spain (+15%), Italy (+8%), Germany (+7%), and several Eastern European destinations continue to demonstrate steady purchasing patterns. Buyers in the region maintain a cautious and disciplined approach to their buying strategies as the market has firmed since industry estimates were released in May.

The Middle East continues to demonstrate resilience despite ongoing geopolitical uncertainty and logistical challenges. Regional shipments remain largely in line with prior-year levels, trailing only 1% year-over-year, as trade flows adjust and buyers continue to secure coverage through alternative channels where necessary. Turkey has unquestionably emerged as the primary throughput destination with Jebel Ali sidelined.

The domestic market shipped 48.2 million pounds, bringing the year-over-year decrease to 13.6%. The 5.5% decline for May was primarily driven by weaker manufactured shipments. New sales for the month were a bright spot as buyers looked to cover current crop needs, increasing forward commitments by 7.19%. While the monthly shipments were lighter than expected the 172 million pounds in commitments has positioned the domestic market to meet the 101 million pounds shipped last year in the final two months. Buyers have been evaluating their needs for new crop and are expected to begin increasing coverage over the next month.

Total commitments currently stand at 438 million pounds, pacing ahead of last year by 8.9%. New sales for the month were impressive, coming in at 138.7 million pounds, up from 89 million pounds last year. The domestic market secured 20.6 million pounds, while exports added 118.1 million pounds of new coverage. Total commitments for the domestic market are now at 172 million pounds while exports have reached 266 million pounds. Stronger sales for the month have reduced uncommitted inventory, now down 5.2% at 469.5 million pounds versus 495.2 million pounds prior year.

New crop sales were reported at 92 million pounds, up 40% from the prior year’s 65.7 million pounds. The domestic market has booked 21.2 million pounds, mostly flat against the prior year’s 20 million pounds, while exports are sitting at 70.8 million pounds, up from prior year’s 45.7 million pounds.

Weather conditions varied over the course of May including temperature variation, strong winds, and rain with losses remaining limited and localized. The 2026 almond crop remains approximately 10 days ahead of prior year, with kernels fully solidified across all varieties. Attention is now shifting toward hull split and navel orangeworm management, with early maturing varieties expected to begin splitting during the week of June 21. There is still concern surrounding disease pressure caused by late spring rains that won’t be realized until harvest.

We will share a more in-depth report surrounding 2026 crop potential in our July Crop Forecast Report.

The May Position Report provided further evidence of the resilience of global almond demand. Export shipments exceeded previous year’s levels. Strong commitment levels, lower uncommitted inventory, and continued buyer participation despite higher replacement values suggest that global demand remains engaged as the industry approaches harvest. While buyer behavior remains measured in certain regions, particularly those facing currency and economic pressures, the industry continues to demonstrate the ability to move volumes across a broad and diversified customer base. This is evident from the strength throughout Europe, Southeast Asia, Turkey, and Morocco, along with several emerging export markets.

As attention shifts toward the new crop, the market will remain focused on summer growing conditions, buyer coverage positions, and the pace of California sales. Most publicly available crop estimates have clustered within a relatively narrow range, reducing uncertainty surrounding overall supply while shifting attention toward quality, sizing, and harvest conditions. While regional demand patterns remain mixed, the overall supply and demand balance continues to support a generally stable market environment as the industry moves closer to harvest.

Senior Sales Director Nut Ingredients

Senior Key Account Manager Global Partner