Gain more insights into the upcoming harvest 2026!

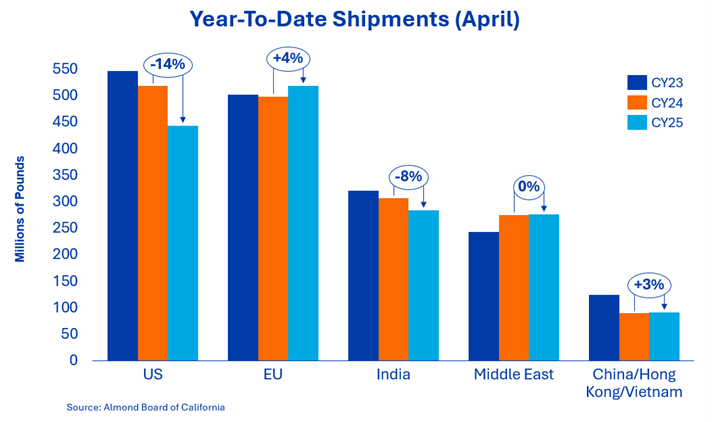

For the month of April, India imported 31.6 million pounds, a significant reduction from last year’s 45.9 million pounds. Compared to last year, the gap has widened to 8%. The market has taken a step back as warmer temperatures have reduced local consumption. India remains a strong player for global inshell consumption and will need to re-engage to secure inventories ahead of new crop supply.

April 2026 shipments to China/Hong Kong totaled 3.7 million pounds, marking a 110% increase compared to prior year. Shipments to Vietnam reached 4.8 million pounds, down 34% for the month and up 46% year to date. Combined shipments to these regions increased 2.65% year to date.

Europe took a slight step back this month, with its growth rate declining year over year from 7% to 4%. The market continues to be a solid performer and reliable outlet for California almonds. Buyer mentality has not changed all year. Calculated and cautious buying activity should be expected to continue through the end of the crop year, with many beginning to shop for new crop coverage. Spain (+17%), Italy (+9%), and Germany (+4%) continue to lead the region’s growth.

The region continues to be hampered by the conflict in Iran. Buyers in the Persian Gulf region continue to take a wait-and-see approach with little appetite for risk. Demand is still present across the region, but logistical challenges and increased transportation costs make it difficult to take positions. Trade flows continue to evolve with new destinations now serving as trade hubs with Dubai unable to participate. Turkey continues to show strength, up 35%, while Pakistan, now up 202%, has emerged as a new throughput option to service the region’s demand. Trade will always find a way if buyers want to engage, but until a resolution is reached, the industry will continue to define a new normal over the coming weeks and months.

The domestic market shipped 52.6 million pounds, resulting in a decrease of 1.3%. April was the second largest shipment month of this crop year, bringing the market year-over-year decrease to 14.4%. Softer monthly sales have led to forward commitments declining by 5.2%. After a long period of steep declines, it appears the domestic market is maintaining its new monthly shipping average just shy of 50 million pounds. With forward commitments of 199 million pounds, this market is well positioned to match prior year’s final quarter shipments of approximately 152 million pounds.

Total commitments currently stand at 517 million pounds, trailing last year by 1.6%. New sales for the month were subdued in anticipation of the Subjective Estimate and totaled 160.7 million pounds, down from 192.5 million last year. The domestic market secured 39.9 million pounds, while exports added 120.8 million pounds of new coverage.

Total commitments for the domestic market are now at 199.6 million pounds while exports have reached 317 million pounds. With softer sales for the month, uncommitted inventory is currently up 4.2% at 605.8 million pounds versus 581.5 million pounds prior year.

The Blue Diamond crop estimate is closely aligned with similar estimates by the USDA Subjective Estimate (2.7 billion pounds) and others in the industry. We will continue to share crop updates in our June Market Report and our July Crop Forecast Report to provide a more precise forecast as we progress through harvest.

Die Prognose beschreibt einen insgesamt ausgeglichenen, aber vorsichtigen Ausblick und berücksichtigt Wetterrisiken, aufgegebene Plantagenflächen sowie sommerliche Bedingungen, die entscheidend dafür sein werden, ob das Ertragspotenzial erreicht wird. Die Schätzung von Blue Diamond liegt sehr nahe an den Prognosen des USDA („Subjective Estimate“) sowie weiterer Marktteilnehmer, die ebenfalls rund 2,7 Milliarden Pfund erwarten. Blue Diamond kündigte an, weitere Ernte-Updates im Juni-Marktbericht sowie im Juli-Ernteprognosebericht zu veröffentlichen, um die Schätzungen mit Fortschreiten der Ernte weiter zu präzisieren.

Overall, the market outlook for the final months of the season remains positive, supported by strong global demand, and well-balanced supply, which is expected to stabilize pricing heading into new crop. We anticipate consistent performance from the domestic market for the remainder of the season, and despite the challenges in trade flow given the geopolitical environment, exports continue to put on a strong performance year to date.

Final shipments for the crop year should result in a manageable carryout. Consistent estimates for the 2026 crop paint a similar picture to 2025, dictating a well-balanced market. Disciplined selling and buying behaviors should lead to a market that is stable to firm, providing a runway for consistent booking activity throughout the crop year.

Senior Sales Director Nut Ingredients

Senior Key Account Manager Global Partner