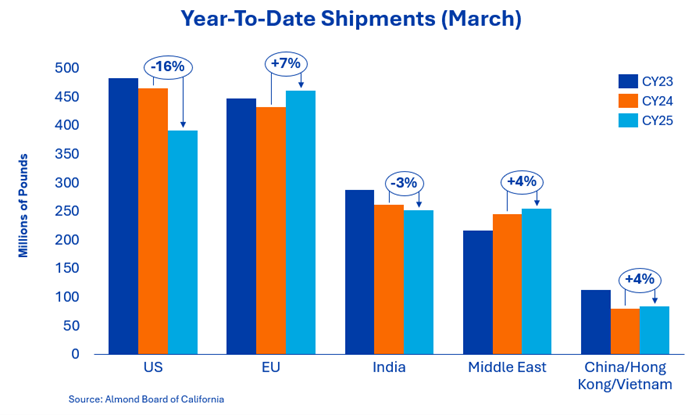

In March, India imported 39.2 million pounds, reducing the year-on-year shortfall to just 3 %. The market continues to absorb significant volumes, although recent shipments have reduced the short-term urgency. India remains an important outlet for global supply, particularly in-shell nuts, and is expected to regain prominence as stocks reduce.

Shipments to China/Hong Kong totaled 4.1 million pounds in March, an increase of 123 % compared to the weaker prior year figure, which was due to the newly introduced tariffs. Shipments to Vietnam reached 5.6 million pounds, an increase of 8.5 % month-on-month and an increase of 63 % year-to-date. Combined shipments to these regions increased by 39 % year-on-year, bringing the overall year-to-date performance into positive territory with growth of 3.7 %. Quality concerns regarding the Australian crop could prompt buyers in the region to source larger volumes from California in the coming months.

This market continues to develop stably with monthly delivery volumes of 77.2 million pounds, which corresponds to a month-on-month increase of 47 %. Since the beginning of the year, delivery volumes are now 7 % higher than last year. Buyers continue to be active, albeit cautious, and are mainly covering their short-term needs, as they have been all year. The region is expected to play an important role in maintaining current supply volumes.

The conflict in Iran has been a worrying factor for the industry for over a month. The March report shows that demand across the Middle East continues unabated as the region took 21.9 million pounds that month. The current geopolitical conditions have caused disruption and logistical challenges for traditional trade flows in the Persian Gulf. While some markets, including the United Arab Emirates, have seen reduced activity, other channels, notably Turkey (+30 %) and Pakistan (+170 %), have seen increased volumes, suggesting that demand is not slowing, but rather redistributing. Saudi Arabia is also expected to act as an alternative route for supplying regional customers. The region remains an important source of demand with creative implementation strategies, and the normalization of logistics should support future activity.

In March, the domestic market broke its streak of month-on-month declines since November 2024 with a shipment volume of 52.8 million pounds. This led to an increase of 1.9 %. It was the highest shipping month of the crop year and symbolically significant as March of the previous year was the first month of double-digit year-over-year declines. Year-to-date shipments are down 15.9 % overall, but a strong booking month has resulted in forward contracts increasing by 3.8 %. The challenges for this market have not yet been overcome. With forward contracts over 212 million pounds, more bookings expected, and a normalizing shipping pace of around 49 million pounds per month, the domestic market should be able to match the shipping pace of the last four months of the last crop year.

Total commitments currently stand at 576 million pounds, an increase of 0.43 % on the previous year. New sales for the month were strong, totaling 240.6 million pounds, up on last year’s 217.6 million pounds. The domestic market secured 45.5 million pounds, an increase on last year’s 34.2 million pounds. Exports recorded an increase of 195.1 million pounds in new contracts, compared to 183.3 million pounds in the previous year.

Total commitments to the domestic market now stand at 212 million pounds, while exports have reached 364 million pounds, which continues to provide a solid base for upcoming deliveries. Uncommitted stocks have been reduced by 0.43 % year on year and stand at 763 million pounds compared to 766 million pounds last year. Looking back to the beginning of the season, the Almond Board of California’s survey of the edible portion of carryover stocks showed that 36 million pounds of carryover stocks were inedible, indicating potentially tighter supplies this crop year.

Crop yields for 2025 are expected to be around 2.69 billion pounds, with the focus now shifting to the 2026 harvest. Above-average temperatures early in the season and intermittent weather events have led to some uncertainty regarding fruit set and grain size. In addition, fuel and fertilizer costs have increased due to the conflict in the Middle East, and water availability is limited due to low snowpack and the implementation of the SGMA law.

Water availability and the economic situation of growers will continue to shape their decisions for this season and ultimately influence harvest potential. Conditions in the coming weeks to months will be critical in estimating yields and quality. Several estimates will be released in the coming weeks that will provide additional forecasts and perspectives, including LandIQ’s first acreage estimate for 2026 on April 23 and NASS’s subjective estimate on May 12.

The delivery trend in March confirmed that the market is functioning smoothly, with global demand continuing to absorb supply at a steady pace. Export markets remain the key driver, supported by steady shipments to Europe, South East Asia and key distribution channels in the Middle East, despite the recent disruption. Developments in the domestic market have been encouraging this month and the industry will continue to monitor the situation.

Buying behavior remains disciplined, with most customers sticking to their short-term demand coverage strategies. Looking ahead, market direction in the coming months will be increasingly influenced by shipping performance and early indicators for the 2026 harvest. With flowering now complete and the industry entering the crop establishment and development phase, attention will increasingly shift to crop potential and core size, which could bring additional momentum as the season progresses.

The market is expected to remain stable to firm due to balanced fundamentals leading to a manageable overhang. The continued processing of deliveries and the normalization of global trade flows will be crucial to maintaining the current market balance.

Senior Sales Director Nut Ingredients